The self-managed superannuation fund (SMSF) sector has established itself as an important and enduring part of the Australian superannuation system with over 1.1 million Australians choosing to use an SMSF to manage their retirement savings. This article provides an overview of the current state of the SMSF sector and assesses challenges that lie ahead for the sector.

The self-managed superannuation fund (SMSF) sector has established itself as an important and enduring part of the Australian superannuation system with over 1.1 million Australians choosing to use an SMSF to manage their retirement savings. This article provides an overview of the current state of the SMSF sector and assesses challenges that lie ahead for the sector.

SMSF Sector Overview

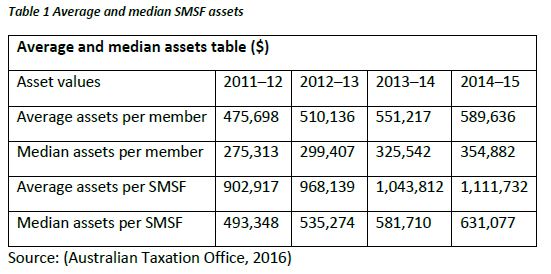

The SMSF sector has grown to 590,742 funds with 1,120,117 members and approximately $675 billion in funds under management, representing close to a third of all superannuation assets (Australian Taxation Office, 2017). As of the 2015 financial year SMSFs had average assets of approximately $1.1 million.

SMSF sector growth

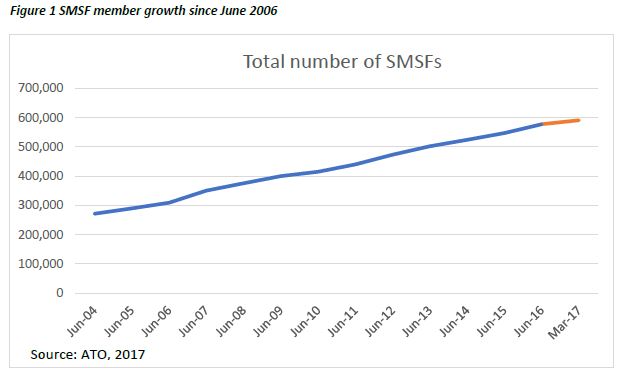

The growth in the number SMSFs has represented a doubling of the number of individuals who are a member of an SMSF since June 2006 and a tripling of assets held by SMSFs in that time. This paints a positive picture of an SMSF sector that has continued to attract new SMSF members and a growing asset base to support member’s retirement income.

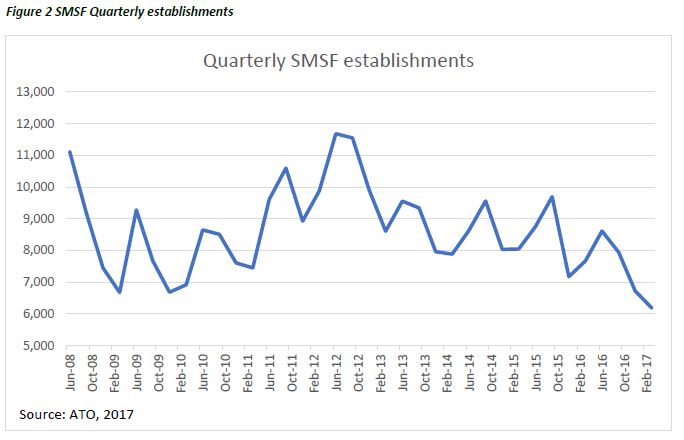

While SMSF growth has been significant over the past decade, growth has been more modest recently. For much of this time the sector has seen quarterly SMSF establishments of 8,000 funds per quarter whereas since 2015, quarterly establishments have fallen. However, growth in numbers of SMSFs for financial years 2015 and 2016 still totalled a healthy 4.4% and 5.5% increase in the number of SMSFs respectively (Australian Taxation Office, 2017).

The softening in SMSF growth numbers can be largely attributed to legislative uncertainty over this time, with significant speculation concerning superannuation tax concessions occurring from the time the Abbott Government launched its Tax White Paper Process. Even following the 2016 Federal Budget, speculation and debate around superannuation changes continued throughout and after the 2016 Federal election until legislation was introduced in Parliament.

With a more stable legislative environment for superannuation going forward, it will be interesting to watch whether SMSF establishment numbers will increase again or remain flat.

SMSF sector demographics

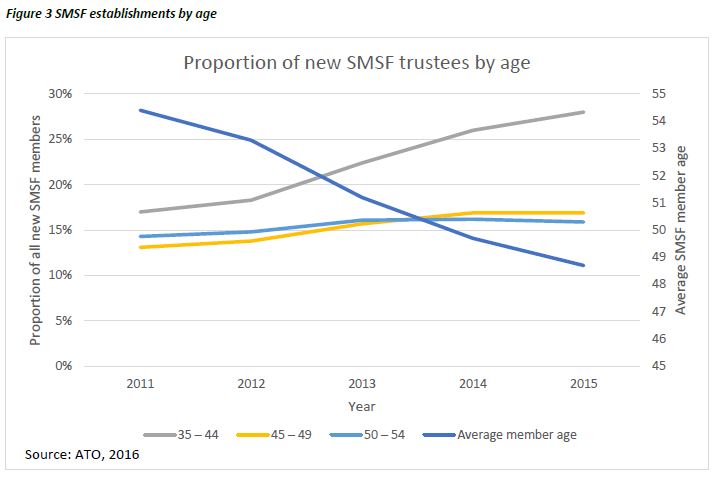

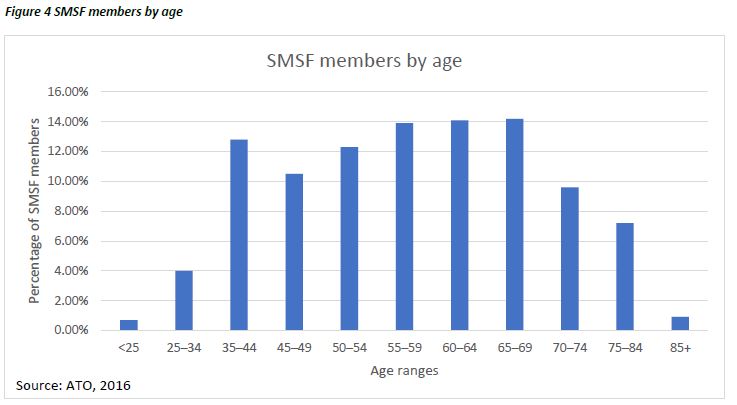

A positive for the SMSF sector has been the increase in new SMSFs from younger trustees. The last six years has seen a significant increase in establishments of SMSFs from people aged between 35-44. In 2011, 17% of new SMSFs were established by people aged between 35-44, while in 2015 28% of SMSFs were established by people in this age bracket (Australian Taxation Office, 2016). This has seen a shift from people using SMSFs as a savings vehicle in preparation for retirement (making large “catch-up” contributions to their SMSF) to one which people view as their chosen vehicle for accumulation and drawdown.

While this new member growth from younger trustees is positive, SMSF members are an aging demographic. As of June 2016, 51.4% of SMSF members were aged between 55 and 75. This will present a number of challenges as the SMSF sector shifts towards having a significant percentage of members in retirement phase drawing down on their assets. New thinking around financial advice in retirement phase, asset allocations and more sophisticated approaches to managing retirement income will be needed.

SMSF assets

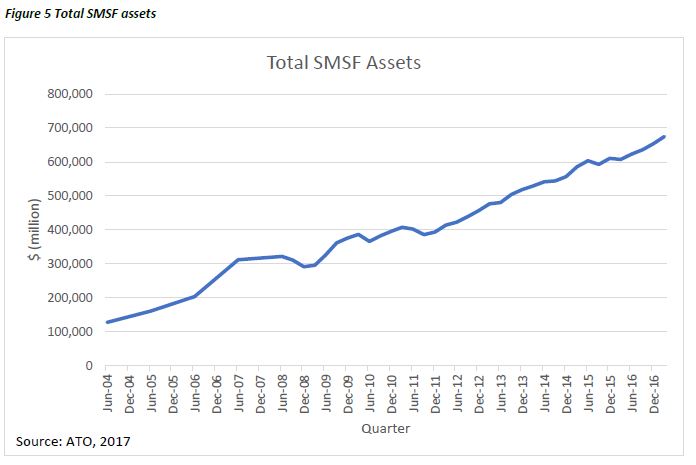

SMSF assets reached $674.7 billion as of March 2017 (Australian Taxation Office, 2017). This has seen SMSF assets continue strong growth since the Global Financial Crisis, averaging quarterly growth of 2.6% over the last eight years since March 2009.

SMSF asset allocation has remained steady over time with a significant proportion of SMSF assets invested in listed shares and cash investments. This persistent feature of SMSF asset allocation has been a source of significant commentary and analysis. The key drivers for this asset allocation include:

- Tax preferences for domestic equities – fully refundable franking credits increase the after-tax return for domestic equities for SMSFs, especially those in retirement phase.

- A desire for liquidity to pay pensions in retirement – this is especially relevant to the SMSF sector where 48 % of funds are in retirement phase (Australian Taxation Office, 2016).

- Cognitive biases which drive allocation to assets which trustees are familiar with, especially blue-chip ASX listed

It is also important to realise the limitation of the ATO statistics which underlie these figures, with many international focussed listed investments such as ETFs and LICs being listed as domestic listed shares, potentially understating SMSF’s international asset exposure. However, improved diversification of SMSF portfolios is an ongoing challenge that the SMSF sector should consider.

Property investment and borrowing

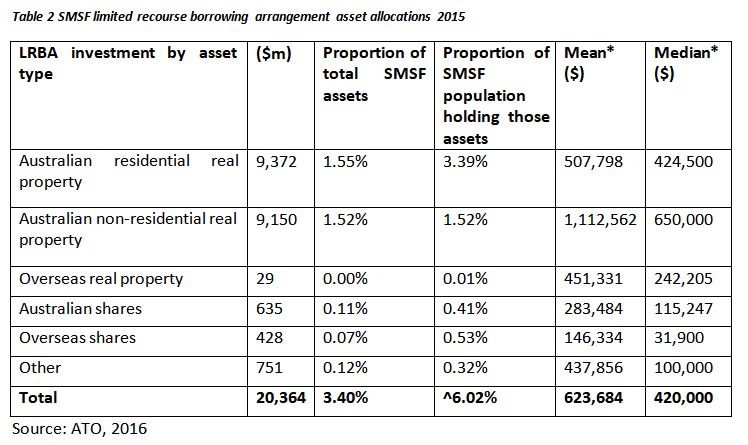

An aspect of asset allocation that often draws significant attention is SMSF investment in unlisted property, especially residential property funded through limited recourse borrowing arrangements (LRBAs).

As of the March 2017 quarter, SMSFs had $78.2 billion invested in non-residential domestic property and $28.2 billion in residential domestic property, representing 11.6% and 4.2% of total SMSF assets respectively (Australian Taxation Office, 2017).

The use of LRBAs is a perpetual source of interest in SMSFs, especially since the Financial System Inquiry investigated their usage and recommended that they be prohibited from further use by superannuation funds in 2014. The then Abbott Government rejected the recommendation and this position has been maintained by the current Government. The Australian Labor Party has recently announced that it will prohibit new LRBAs if elected.

While the use of LRBAs has grown significantly they still only represent a very small proportion of SMSF assets (3.8%) held by a small overall number of SMSFs.

The use of LRBAs to invest in residential property has received criticism for contributing to a potential Australian housing bubble. However, this critique seems unjustified given that SMSFs hold $28.2 billion of Australia’s $6.6 trillion total dwelling stock (Australian Bureau of Statsitics, 2017) – only 0.42% of the entire housing market.

Furthermore, ATO data from the 2015 income year shows that the use of LRBAs is almost evenly split between funding residential and non-residential property, contradicting the theory that all LRBAs are being used to speculate on Australia’s red-hot housing market.

Challenges ahead

Superannuation legislation

The changes to the superannuation tax settings made in the 2016 Federal Budget which took effect on 1 July 2017 represent the most significant changes made to superannuation in a decade. The key changes affecting SMSFs are:

- Lower concessional and non-concessional contribution caps.

- A $1.6 million “transfer balance cap” on assets in retirement phase that benefit from earnings exempt from

- Removal of the tax exemption for earnings from assets supporting transition to retirement income streams (TRIS).

The changes present two key challenges for the SMSF sector going forward:

- An increase in complexity of superannuation laws, especially for those with higher

- A limit on contributions to superannuation.

Complexity

The changes to the superannuation laws, especially the introduction of the transfer balance cap, has resulted in a significant increase in complexity for individuals affected by the changes. The changes have increased the need for professional advice and assistance with compliance.

Changes to the contribution caps are the simplest for individuals to comply with as annual limits have been reduced. However, even the changes to non-concessional contributions have detailed transitional arrangements for those who have used the “bring forward” provisions and have a superannuation balance between $1.3 million and $1.6 million.

Similarly, changes to TRISs are relatively simple but transitional capital gains tax (CGT) relief for affected assets and broader strategic considerations of maintaining a TRIS creates complexity.

The introduction of the transfer balance cap is the most complex change for SMSFs to contend with. The transfer balance cap functions on a basis of credits and debits that limits the amount of assets held in retirement phase to $1.6 million. While simple in concept, the reality of the law is that it applies differently to account based pensions, market-linked and term-allocated pensions, defined benefit pensions, child pensions and death benefit pensions. In addition, transitional CGT relief for assets affected by the new transfer balance cap adds further complexity as will real-time reporting to the ATO of events that give rise to changes in a transfer balance cap.

The estimates of SMSFs affected by the legislation changes vary but some credible estimates are:

- Transfer balance cap – 8% of SMSFs, 9.9% of SMSF members. (Class Limited, 2017).

- Concessional cap reduction –8% of SMSF members made contributions above $25,000 in the 2015 income year (Class Limited, 2017).

- Non-concessional cap reduction – 6% of SMSF members aged 49 and over contributed above $100,000 in the 2015 income year (Class Limited, 2017)

- TRIS changes – ATO statistics indicate that 21% of SMSF members received a TRIS in the 2015 income year (Australian Taxation Office, 2016).

Less contributions to superannuation

The reduction in both concessional and non-concessional contribution caps will have a longer-term impact on the growth of assets in the SMSF sector. The lower caps will constrain contributions to the sector in the future, slowing the growth rate of SMSF assets. (However, the carry forward of unused concessional cap space will allow individuals with under $500,000 in superannuation to make additional contributions).

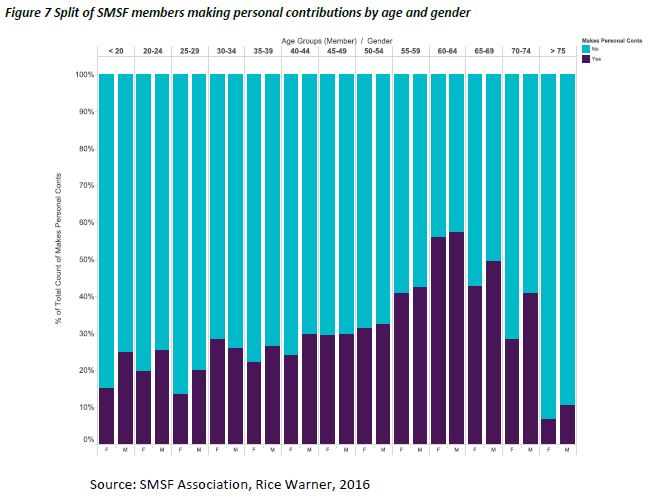

For individual SMSF members, lower contribution caps will result in a reduced ability to make top-up contributions to their superannuation, especially later in life. SMSF Association-Rice Warner research illustrated the prevalence of higher personal contributions to SMSFs later in a person’s life (SMSF Association, 2016).

Investment allocation

SMSFs remain heavily weighted to their traditional asset allocation of Australian equities, cash and property as illustrated above in ATO asset allocation statistics. This has stood SMSFs well over the past decade with Rice Warner finding that SMSFs have outperformed their APRA-regulated counterparts in eight out of twelve years between 2005 and 2016 (Rice Warner, 2017). However, this asset allocation should be questioned going forward.

SMSFs should be considering increasing their portfolio diversification by increasing exposure to:

- Different markets to reduce home bias.

- Different market sectors to better harness the benefits of economic growth in new industries (e.g. greater exposure to technology companies not found on the ASX)

- Different asset classes, especially fixed interest and bond investments.

SMSFs should also consider and understand the risk they are accepting for their asset allocation’s return. Research by Vanguard has shown that the risk of a typical SMSF that aspires to have a “growth” asset allocation doubles that of a diversified growth fund (Bowerman, 2014). If this level of risk is unintended (which it most likely is), then SMSF trustees and their advisors should be considering greater diversification away from Australian equities and cash to reduce the risk and volatility of their investments.

Ultimately, this may be a financial advice challenge for advisors servicing SMSFs.

Retirement income

As a significant percentage of the SMSF sector moves towards retirement phase, the ability for SMSFs to deliver stable, long-term retirement income will be put under the microscope.

To date, SMSFs have been successful in providing retirement income to members with 94% of all benefits taken from SMSFs being in the form of an income stream (Australian Taxation Office, 2016). This is dominated by account based pensions. SMSFs have had a very low uptake of retirement income products that can be used to provide stable income and insure against longevity risk.

With the development of comprehensive income products for retirement (CIPRs) the SMSF sector may benefit from a deeper pool of retirement income products and also be challenged to innovate and look at greater sophistication in drawdown phase. Greater depth of available products and competition for SMSF/retail investors may deliver more attractive product options for SMSFs, which could lead to an increase in the take-up of retirement income products by SMSFs

As the SMSF demographic shifts, greater attention will need to be paid to asset allocation in retirement, including self-insuring against longevity risk by using a “pooled” or “bucket” approach for investing assets to provide current income, flexibility to access capital and manage longevity risk.

Aging SMSF Member Population

The SMSF sector has a significant number of members who are either beginning retirement or retiring in the next 20 years with 51.4% of members aged between 55 and 75. In addition to the need to consider changing investment and retirement income strategies, this demographic shift poses additional challenges associated with aging.

The key challenges stemming from aging include:

- The effects of aging and cognitive declines causing individuals to lose capacity to be a trustee of an

- Increased disputes over death benefit payments from SMSFs.

Loss of capacity

This issue of loss of capacity to be a trustee was recently cited as an emerging risk for the SMSF sector in the Australian Law Reform Commission (ALRC) review of elder abuse which culminated in the ALRC’s report “Elder Abuse – A National Legal Response” (Australian Law Reform Commission, 2017).

Where an SMSF trustee loses the capacity to be a trustee of an SMSF (or a director of a corporate trustee of an SMSF) the SMSF will become non-compliant unless certain management steps are taken. A common strategy to overcome this issue is for the trustees of the fund (or directors of a corporate trustee) to have an enduring power of attorney (EPOA) in place, and the attorney can step into their role in managing the SMSF.

However, this arrangement can create a number of risks including elder abuse by the attorney and also legal complications with replacing the trustee who has lost capacity with their attorney (this issue is not as common for corporate trustees where a change of directors occurs). These complications can be exacerbated when there has been poor planning for succession of trusteeship. The ALRC Report made a number of recommendations to curb these emerging risks around loss of capacity and trusteeship including:

- Introducing new safeguards against the misuse of

- Introducing ‘replaceable rules’ for SMSFs into the Superannuation Industry (Supervisory) Act 1993 which provide a mechanism for an attorney to become trustee/director where the EPOA allowed for it but the fund’s trust deed does not

- Introducing an additional operating standard in the Superannuation Industry (Supervisory) Regulations 1994 for SMSFs requiring them to consider planning for loss of capacity as part of their overall investment

- Requiring an attorney who becomes a trustee of an SMSF to notify the ATO they are doing so as a consequence of an

These reforms are sensible adjustments to the existing superannuation laws that mitigate risks of losing capacity and elder abuse without over regulating SMSFs. In addition to these reforms, SMSF advisors need to be aware of the risks associated with aging SMSF trustees and ensure their clients are advised and have appropriate strategies in place to meet these challenges later in life.

Death benefit disputes

As the SMSF population ages more death benefits will be paid out from SMSFs. In the 2015 income year 12.5% of lumps sums and 0.8% of income streams paid from SMSFs were death benefits (Australian Taxation Office, 2016). These figures have the potential to increase substantially as the SMSF demographic ages and the transfer balance cap forces more superannuation money out of the system. With increased death benefit payments from SMSFs there comes potential for increased potential for disputes and litigation over SMSF death benefits.

Already there has been a substantial increase in litigation over SMSF death benefits in recent years. This mirrors the increase in complaints to the Superannuation Complaints Tribunal (SCT) over death benefit payments in recent times. The SCT cites 21.5% of all complaints in the March 2017 quarter related to distribution of death benefits (Superannuation Complaints Tribunal, 2017). This trend will continue and grow as more death benefits are paid.

SMSF trustees seeking specialist SMSF and estate planning advice is a crucial factor in mitigating the risk of death benefit disputes. Trustees need professional assistance in ensuring that binding death benefit nominations are drafted correctly and that SMSF trust deeds are structured properly to allow for appropriate succession of trustees so that death benefits are paid in accordance with the deceased member’s wishes.

The ALRC’s Report also dealt with this issue (albeit from an elder abuse perspective) and has recommended a review of the superannuation death benefit provisions to clarify their application. This would be a welcome review given the increase in death benefit disputes arising in SMSFs, and superannuation more broadly.

Advice to SMSF trustees

Financial advice is a key driver of a well-functioning SMSF sector. Ensuring SMSF trustees are receiving high quality advice is accordingly essential.

This will be supported by the new education and ethical standards for financial advisors which will be created by the new Financial Adviser Standards and Ethics Authority and backed by legislation and broad industry support. The new regime will mean that new professional standards for all advisers who operate in the SMSF space will be introduced over a period of time.

New financial advisers will need to meet minimum education and exam requirements from 1 January 2019. In addition, a supervision year will commence for new entrants. A new code of ethics is to apply to all financial advisers from 1 January 2020. All financial advisers will be required to pass an exam by

1 January 2021 and have achieved degree qualifications by 1 January 2024. All of these changes impact all advisers who are providing advice which requires licensing under the Corporations Act.

In addition to the new standards, advice challenges for the sector continue around providing retirement advice with SMSF Association-Commonwealth Bank research showing that this as well as pension strategy/management and providing clarity around investment research and products were key areas advisors could assist trustees with (SMSF Association, CommBank, 2017).

By: Jordon George – Head of Policy – SMSF Association http://www.smsfassociation.com/

References

Australian Bureau of Statsitics. (2017, June 20). 6416.0 – Residential Property Price Indexes: Eight Capital Cities, Mar 2017. Retrieved from Australain Bureau of Statistics Website: http://www.abs.gov.au/ausstats/abs@.nsf/mf/6416.0

Australian Law Reform Commission. (2017). Elder Abuse – A National Legal Response. Sydney: Commonwealth of Australia.

Australian Taxation Office. (2016, December 20). Australian Taxation Office Website. Retrieved from Self-managed superannuation funds: A statistical overview 2014-2015: https://www.ato.gov.au/Super/Self-managed-super-funds/In-detail/Statistics/Annual- reports/Self-managed-superannuation-funds–A-statistical-overview-2014-2015/

Australian Taxation Office. (2017, June 23). Self-managed super fund statistical report – March 2017.

Retrieved from Australian Taxation Office Website: https://www.ato.gov.au/Super/Self- managed-super-funds/In-detail/Statistics/Quarterly-reports/Self-managed-super-fund- statistical-report—March- 2017/?anchor=SMSFpopulationtableannualdata#SMSFpopulationtableannualdata

Bowerman, R. (2014, April 4). The risk and return of SMSFs. Retrieved from Vangaurd Investments Australia: https://www.vanguardinvestments.com.au/au/portal/articles/insights/commentary/The- risk-and-return-of-SMSFs.jsp

Class Limited. (2017, March). March 2017 SMSF Benchmark Report – Impact of the Super REFORMS. Retrieved from Class Limited Website: https://www.class.com.au/wp- content/uploads/2017/05/CLS17-3139_Benchmark_March_2017_WEB.pdf

Rice Warner. (2017, March 9). In Defence of the SMSF Investor. Retrieved from Rice Warner Website: http://ricewarner.com/in-defence-of-the-smsf-investor/

SMSF Association, CommBank. (2017). The SMSF Report. Retrieved from Commbank Website: https://www.commbank.com.au/personal/superannuation/smsf/smsfreport.html

SMSF Association, R. W. (2016). SMSF Association research into SMSF contribution patterns. – Adelaide: SMSF Association.

Superannuation Complaints Tribunal. (2017, March). SCT Quarterly – Q1 2017. Retrieved from Superannuation Complaints Tribunal Website: http://www.sct.gov.au/newsletters/sct- quarterly-q1-2017

You must be logged in to post a comment.